Introduction

Today’s discussion on the future of healthcare revolves less around arguments regarding medical technology, and more surrounding economic challenges. Scarce resources, government budget constraints and limited to no access to the capital market offset various cost drivers.

In addition, a global trend towards population health management exists, an integrated optimization of healthcare that greatly impacts processes and business models and requires the comprehensive aggregation and analysis of patient data. This is Health 4.0, the increasing standardization and industrialization of patient care.

In addition, a global trend towards population health management exists, an integrated optimization of healthcare that greatly impacts processes and business models and requires the comprehensive aggregation and analysis of patient data. This is Health 4.0, the increasing standardization and industrialization of patient care.

All over the world, top managers of healthcare facilities face scarce resources, economic and regulatory uncertainty and increasing market volatility. Trends such as alternative compensation models, public-private partnerships and new, lucrative patient flows from abroad (medical tourism) cause people to rethink established business models and adapt their investment strategies. Most players will need to develop new business models to win, the consulting firm Bain & Company predicts.1 Deloitte consulting adds, Many of these new models will require costly infrastructure investments.2

Investing During Difficult Times

Investing During Difficult Times

The lion’s share of medical costs is incurred during treatment. Rapid, accurate diagnoses and effective therapy management and control can significantly reduce these costs. They point the way to optimal treatments, reduce unnecessary readmissions of patients, and are a valuable aid in prevention. The use of modern diagnostic technologies in imaging and laboratory can help achieving this goal.

At first glance, the required investment may appear to be a financial hurdle. But investing continuously in effective and efficient medical technology, as well as in systematic and continuous training of staff, contributes decisively to the proper management of diagnosis and treatment. This helps hospital operators reduce costly mistakes and opportunity costs, and therefore substantially improve their cost structure for the long term.

The basis for commercial success depends on an accurate evaluation of one’s equipment needs, rather than assessing past or upcoming investments primarily based on isolated cost targets. A comparison of the usage behaviour of individual companies can yield salient insights for the effective use and optimum capacity utilization of all equipment.

Many hospital operators have no or very limited possibilities to obtain financing from the capital market. Flexible, off-balance-sheet and usage-based financing models such as leasing, hiring, or purchasing increasingly offer the ability to convert Capex to Opex, letting operators realize planned investments promptly and with minimal strain on liquidity.

A Growth Market Under Cost Pressure

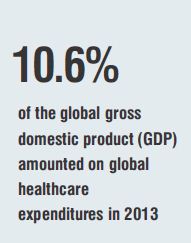

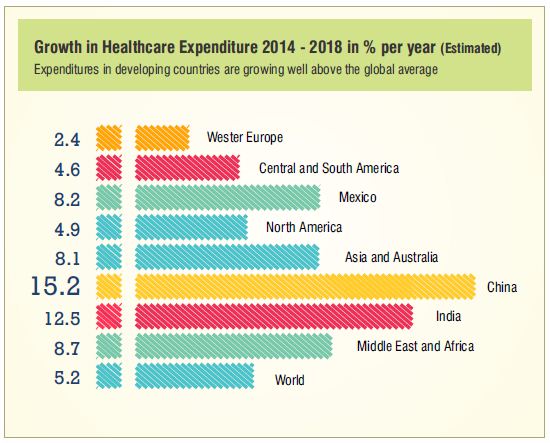

Global healthcare expenditure amounted to approximately 7.2 trillion U.S. dollars in 2013, 10.6 percent of global gross domestic product (GDP). Global expenditure continues to rise – albeit with regional differences (see Growth in healthcare expenditure 2014-2018).

The growing and aging world population, the rise in chronic diseases, a growing middle class in emerging markets and advances in diagnosis and therapy are all key drivers of rising global healthcare expenditure.

However, for hospital operators, rising healthcare expenditures do not automatically translate to an increase in revenues and profits. Rather, faced with higher numbers of patients, they receive pressure to reduce the cost of treatment as health systems increasingly respond to higher overall expenses with cost-capping measures.

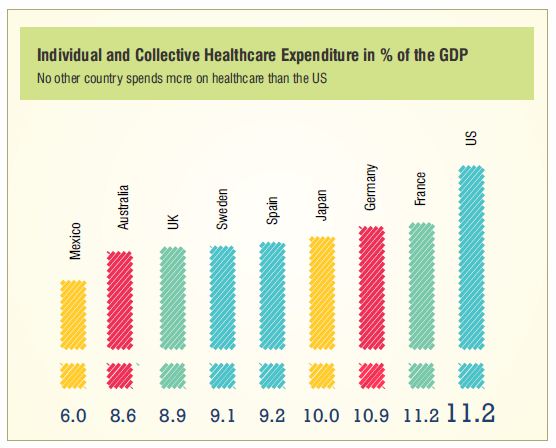

For example, the United States’ per-capita healthcare expenditure is approximately 8,400 U.S. dollars per year, among the highest in the world.3 This corresponds to 16 percent of GDP, and is expected to rise to nearly 18 percent by 2018 according to Deloitte (see Individual and collective healthcare expenditure).

Meanwhile, the cost bearers put further pressure on hospital managers to reduce costs.

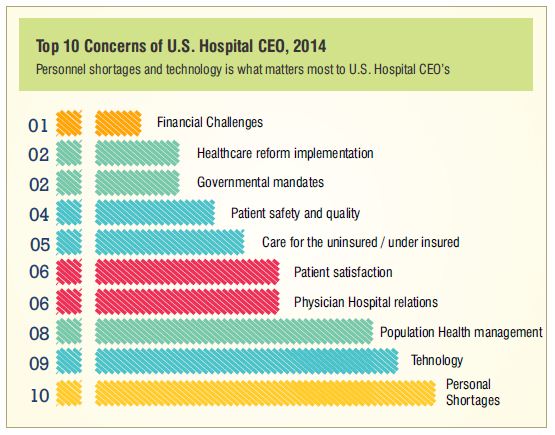

While U.S. healthcare reform the Affordable Care Act (ACA) is designed to reduce the increase in costs, financial challenges are still the biggest headache for U.S. hospital managers (see Top 10 concerns of US hospital CEOs, page 4).4

The positive effects of the ACA for example, more people with health insurance – cannot compensate for the pressure on revenues and margins, especially in the not for profit health sector.3 Moreover, the U.S. Census Bureau predicts stagnant revenues for state specialist hospitals upcoming years.5

Meanwhile, cost bearers (insurance companies, employers) put further pressure on hospital managers to reduce costs. For example, they threaten to reduce remuneration if hospitals readmit patients within certain time limits (readmission programs). Managed Care Plans give hospital operators an annual flat rate for patients – regardless of the services provided.

Hospital operators take on risks formerly managed by insurance companies. This reversal of the value add mechanism, away from a »fee-for-service« model and towards a fee-for-outcome model, changes the significance of investments in medical technology.

Investments in medical technology equipment and provided services used to be decisive for revenues, but now, in these models, they have become an important performance indicator in providers’ cost management.

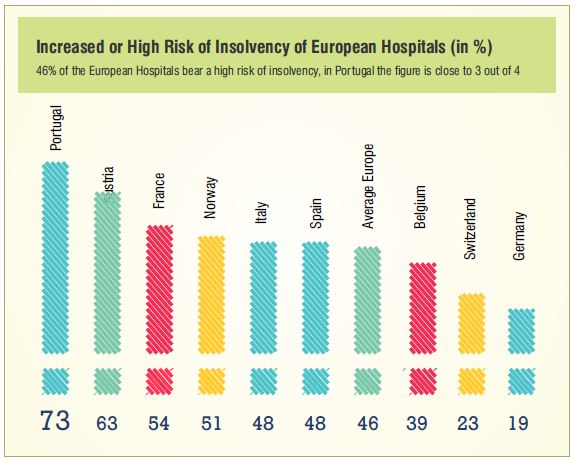

In Europe as well, cost pressure and commercial risks dominate. Nearly half of all European hospitals are in financial difficulties, especially in countries like Greece and Portugal. The industry-specific high risk of bankruptcy complicates hospital operators’ access to the capital market.

Things are more positive in more stable economies such as Germany, Switzerland, and Belgium. In Europe, the profitability of the most commercially successful hospitals has continuously improved, while that of the least successful has continuously deteriorated. According to a study by the Accenture consulting firm, the average EBITDA margin of selected European hospitals amounted to approximately 5% in 2014. Peak values were achieved in Italy (12%), France (11%), and Germany (8.5%). Austria (-4%) and Portugal (-5.3%) brought up the rear.6

Given increasing patient numbers and overall costs in both Europe and the U.S., increased efficiency is becoming an existential concern for hospital operators

Given increasing patient numbers and overall costs in both Europe and the U.S., increased efficiency is becoming an existential concern for hospital operators. Meanwhile,financially sound healthcare companies can consolidate their market position through strategic investments.

Cost Efficiency in Asia

In the search for innovative business approaches, it is worth taking a look at the Far East. In countries like China and India, low per-capita income, a rapidly growing population, uncertain economic prospects, and a shortage of beds and doctors, especially in rural regions, make efficient and affordable provision a special challenge.

For example, in India, the out-of-pocket spending rate is the highest in the world at about 70 percent. At the same time, India is one of the poorest nations in the world.

Narayana Health (NH), one of the world’s least expensive and most rapidly expanding hospital companies, was established in this environment. Since it was founded in 2001, NH has grown from a small cardiology clinic into an internationally renowned major medical company with approximately 6,500 beds in 30 hospitals. Its success is mainly based on a systematic low-cost strategy. This includes the efficient use of modern technology and optimized surgery capacity. In 2014, the Boston Consulting Group named NH as one of the 50 most successful companies in the emerging markets.7

“ For us, looking at a profit and loss account at the end of the month is like reading a post-mortem report. You cannot do anything about it. Whereas if you monitor it on a daily basis, it works as a diagnostic tool. You can take remedial measures. While charity is not scalable, good business principles can be scaled up, and can be taken to any level.” By Devi Shetty, Chairman and Founder Narayana Health

The Medical Tourism Trend

Many of NH’s patients come from abroad, so NH is participating in the worldwide trend of global »medical tourism.« Many successful hospital operators secure lucrative patient flows from abroad with excellent, low-cost services, a good international reputation, and a focus on foreign target groups, especially on wealthy private patients.

Experts estimate that medical tourism has a market size of $ 38.5-55 billion globally, based on approximately 11 million cross-border patients worldwide spending an average of $ 3,500-5,000 per visit.9 A huge market is emerging: It is estimated that 750,000-1.2 million U.S. residents travel abroad for care each year.10 In Germany, according to investigations by Bonn-Rhein-Sieg University of Applied Sciences almost 250,000 foreign patients (including 97,000 stationary patients) are already earning German healthcare facilities 1.2 billion Euros a year in the hospital sector alone.11

Financially sound healthcare companies can consolidate their market position through strategic investments.

Medical tourists are fueled by a variety of motives: many who travel for care do so because treatment is much cheaper in other countries. For instance, the cost of heart surgery at NH averages less than 1,700 Euros ; in the U.K. it is seven to ten times higher.12 Other particularly low-cost countries include Malaysia, Thailand, Mexico, and Turkey.

By the same token, wealthy patients from places like the Middle East or Eastern Europe often seek better medical care abroad

In a nutshell Financial Performance in Healthcare

Efficient service delivery will be the basis of competitiveness for hospital operators worldwide. This calls for solutions that deliver better outcomes in patient care, at lower cost.

1. Innovative, high-performance technology can be of particular service in this. Viewed in isolation, expensive, large equipment is no longer an automatic generator of revenues. However, an accurate assessment of the patient‘s condition significantly enhances the cost efficiency of treatment.

2. New business models increasingly turn hospital operators into risk and population health managers. To assess risks and efficiently manage the costs of service provision, they need reliable diagnostic data more than ever.

3. Access to capital provides a major challenge for many hospital operators. Off-balance-sheet financing of equipment through models like hiring, purchasing, or leasing shifts capital costs to the operational area (Capex to Opex), and thus enables timely investments.

4. In the competition for wealthy private patients and medical tourists from other countries, financially sound companies will manage to defend and expand their competitive position in the future, even across borders.

References:

1 Bain & Company, Healthcare 2020, 2012

2 Deloitte, 2015 Global health care outlook

4 American College of Healthcare Executives, Annual Survey 2014

5 Statista, 2015

6 Accenture, European Hospital Rating Report, 2014

7 BCG Perspectives, BCG 2014 Local Dynamos, 2014

9 Patients Beyond Borders, 2015; www.patientsbeyondborders.com

10 Centers for Disease Control and Prevention; 2015;

www.cdc.gov

11 Hochschule Bonn-Rhein-Sieg 2013, Forschungsgruppe Medizintourismus;

www.fb01.h-brs.de

12 UK National Health Service; in: Deloitte Health Care and Life Science Predictions 202

{kind=link}